Table of Content

Starting with the overnight rate, the MCLR durations extend up to three years, with long duration products like home and auto loans linked to the one-year rate. For such products, banks have a mark-up over the one-year MCLR, depending on the risk perceptions, which becomes the final rate. And Kotak Mahindra Bank, which are currently offering some of the lowest rates in the market. While SBI’s lowest home loan rate is currently at 6.7% per annum, Kotak is charging 6.65% annual interest on its home loans. Home loans at private lender ICICI Bank are currently priced at 6.8%. “This is the best time to buy a home as it gives the aspiring home buyers a lifetime opportunity to purchase their dream home with various festive offers, as well as all-time low interest rates.

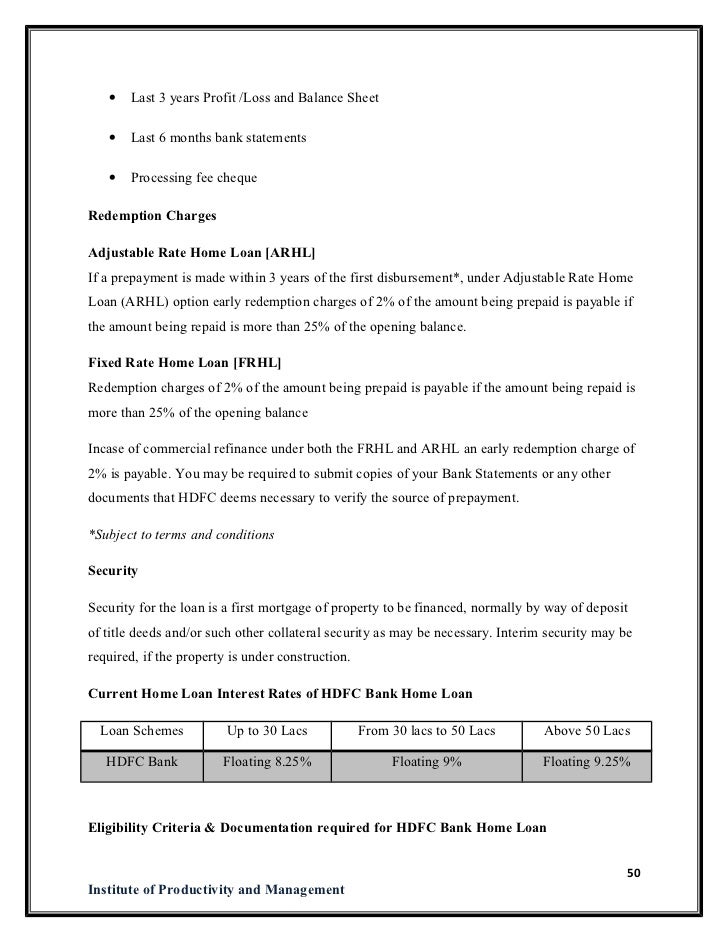

Home loan providers usually charge a processing fee around 0.5% of the loan amount to be availed. Choose a home loan provider who is transparent w.r.t. processing fee and other related charges. Working Capital, Debt Consolidation, Repayment of Business Loan, Expansion of business, Acquisition of Business asset or any similar end usage of funds. Incidental charges & expenses are levied to cover the costs, charges, expenses and other monies that may have been expended in connection with recovery of dues from a defaulting customer. A copy of the policy can be obtained by customers from the concerned branch on request. Fees on account of external opinion from advocates/technical valuers, as the case may be, is payable on an actual basis as applicable to a given case.

What are the different types of Home Loans available in India?

Private sector HDFC Bank has hiked its marginal cost of funds-based lending rate . The one-year MCLR, which acts as benchmark for many consumer loans, has increased by 50 basis points to 8.60 percent, HDFC Bank website said. The rate hike means EMI on a Rs 1-crore housing loan with a 20 year repayment tenure going up from Rs 80,865 a month to Rs 82,404 a month. Since HDFC follows a 3-month cycle for repricing its home loans, the increase would reflect differently for individual borrowers. Repo rate is defined as the rate of interest at which the Reserve Bank of India lends money to commercial banks. Banks avail loans from the central bank by selling eligible securities.

Record low-interest rates, subsidies under the PMAY and tax benefits have also helped.” said Renu Sud Karnad, managing director, HDFC Ltd. These articles, the information therein and their other contents are for information purposes only. All views and/or recommendations are those of the concerned author personally and made purely for information purposes. Nothing contained in the articles should be construed as business, legal, tax, accounting, investment or other advice or as an advertisement or promotion of any project or developer or locality. HDFC joins a number of lenders that have recently raised interest rates, including state-run Punjab National Bank, ICICI Bank and Bank of Baroda.

Home Loan Charges and Feesfor Salaried individuals

Such fees is payable directly to the concerned advocate / technical valuer for the nature of assistance so rendered. The maximum period of repayment of a loan shall be up to 30 years for the Telescopic Repayment Option under the Adjustable Rate Home Loan. For all other Home Loan products, the maximum repayment period shall be up to 20 years. Make sure you provide all the details that the home loan provider will need to process your application. Our chat service on our website and WhatsApp are available 24X7 to assist you with your housing loan related queries.

The loan is structured in such a way that the EMI is higher during the initial years and subsequently decreases in proportion to the income. Improve your credit score by creating a reasonable track record of timely repayments so that you achieve a high credit score which would improve your prospects of getting a home loan. Check your loan eligibility before starting your home loan application. By a cumulative 75 basis points to 5.75%, in three successive steps since February 2019 and prodded banks to pass on the benefits to end-customers, as they have lowered only 21 bps as of June 2019. Industry experts are of the view that that the reduction in home loan interest rates would be greatly beneficial for a sector that has been trying to spring out of a prolonged slowdown. In the last couple of years, property prices have more or less remained the same in major pockets across the country, while income levels have gone up.

HDFC hikes rates by 25 basis points

The prepayment charges are subject to change as per prevailing policies of HDFC and accordingly may vary from time to time which shall be notified on . The Borrower will be required to submit such documents that HDFC may deem fit & proper to ascertain the source of funds at the time of prepayment of the loan. The customer shall pay the premium amounts directly to the insurance provider, promptly and regularly so as to keep the policy / policies alive at all times during the pendency of the loan.

Credit Linked Subsidy Scheme under PMAY makes the home finance affordable as the subsidy provided on the interest component reduces the outflow of the customer on the home loan. The subsidy amount under the scheme largely depends on the category of income that a customer belongs to and the size of the property unit being financed. HDFC disburses loans for under construction properties in installments based on the progress of construction. Every installment disbursed is known as a 'part' or a 'subsequent' disbursement. Our HDFC Reach Loans make home buying possible for micro-entrepreneurs and salaried individuals who may or may not have sufficient proof of income documentation.

Read in other Languages

You can download account statements, interest certificates, request for home loan disbursement and do much more. Effectively, now home loan rates of the lender would start from 7.55 per cent. According to rating agency Care Ratings, the home loan segment continues to be the fastest growing credit segment in India, registering a moderate growth of up to 7.7% in January 2021.

Repayment of home loans is done through Equated Monthly Installments , which is a combination of interest and principal. In the case of loans for resale homes, EMI begins from the month subsequent to the month in which disbursement of the loan is done. In the case of loans for under-construction properties, EMI usually begins once the construction is complete and the house loan is fully disbursed. The EMIs will proportionately increase with every partial disbursement made as per the progress of construction. You can apply for a home loan online from the ease and comfort of your home with HDFC’s online application feature.

Nearly all banks in the country have already increased lending rates with the start of the RBI’s rate hiking cycle, making housing loans more expensive for India’s home buyers. Before the rate cut, the housing finance company was charging between 6.8% and 7.3% interest on its home loans. A number of lenders, including HDFC Bank and Bank of India, hiked their benchmark lending rates after Reserve Bank of India announced a repo rate hike by 35 basis points. As a result, the equated monthly installments of these banks will get expensive for those who avail consumer loans such as home and auto loans against the benchmarks. The housing finance company’s housing loans are provided at its retail prime lending rate, which is linked with the RBI’s repo rate. Several banks and lenders have revised their lending rates after the Reserve Bank of India hiked its benchmark lending rates on December 7.

For those who do not have the required credit score, the interest rate may vary between 8.40 per cent to 8.90 per cent. As a result, new and existing borrowers witness increased loan interest rates. Earlier, HDFC increased its benchmark lending rate by 5 basis points for existing borrowers with effect from May 1. On Wednesday, RBI had increased the key lending rate by 40 basis points and it has now reached 4.40%.

This is the highest housing loans at HDFC have been in the past 2 years. However, rates are still lower than they were before the coronavirus pandemic. As mentioned earlier, the repo rate is used by the central bank of India to control the flow of money in the market. An increased repo rate denotes that the banks who borrow money during this period from the central bank will have to pay higher interest. This discourages the banks to borrow money, which in turn, reduces the supply of money in the market and helps negate the inflation. Lending major Housing Development Finance Corporation has increased its Retail Prime Lending Rate on housing loans -- on which its Adjustable Rate Home Loans are benchmarked -- by 50 basis points.

Hours after the Reserve Bank of India increased the repo rate by 50 basis points on September 30, 2022, several banks in the country, including SBI, ICICI Bank and HDFC, have announced a hike in lending rates. Unlike banks, which automatically pass on any reverse repo rate change, HDFC has the freedom to decide on revising the adjustable rate home loans. However, post-merger with the bank, HDFC Bank too will have to offer repo rate-linked loans to new borrowers. When the repo rate increases, the interest rate at which commercial banks borrow money from the central bank increases and the borrowing becomes costlier. In turn, the commercial banks increase their lending rates to cope up with the hike in the repo rate. Thus, when common men borrow money from the commercial banks, the effective interest rate becomes higher and they end up paying higher interest amounts for the loan that they borrow.

No comments:

Post a Comment